Accessing Kenneth French's US equity data

Kenneth French collects, updates, and makes available a treasure trove of datasets of U.S. American equity markets on his website at http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/. Many of these data are derived from the CRSP database (http://www.crsp.com/).

Since version 1.5, the NMOF package has provided a

function French that helps with downloading datasets

from Kenneth French's website.

In this short note, the function and some of the datasets

that is supports are showcased.

library("NMOF") library("plotseries") library("zoo")

The Fama/French factors

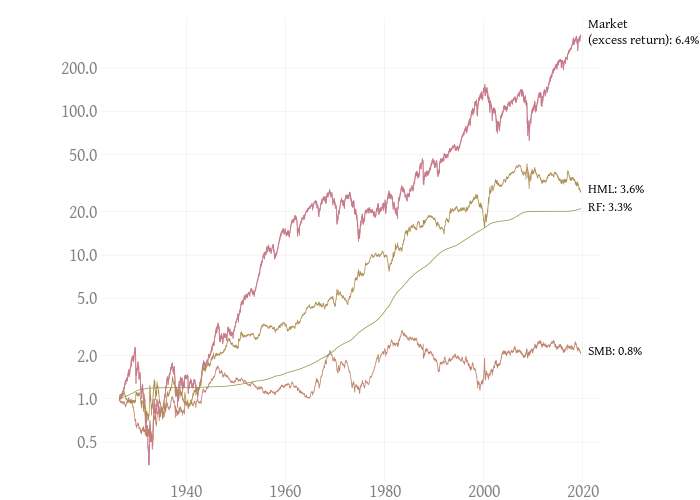

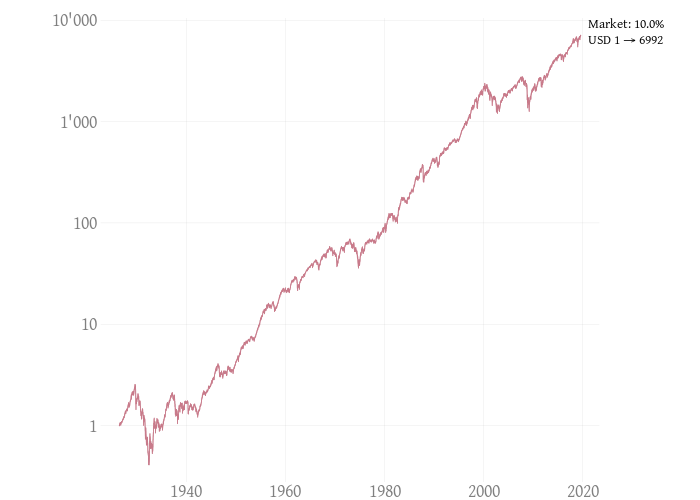

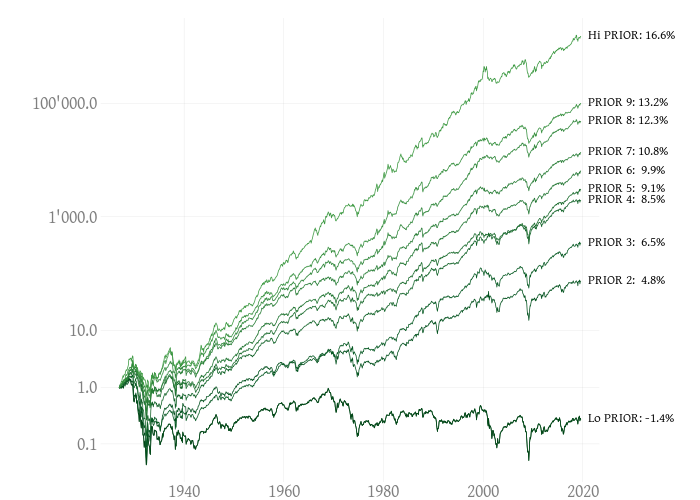

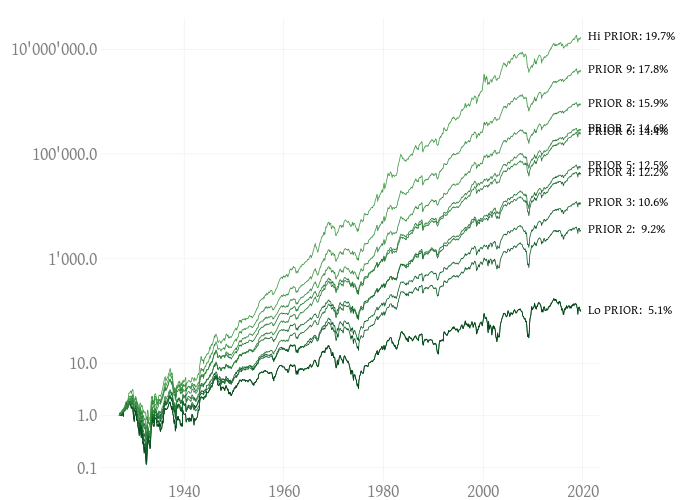

The numbers in the right margin are the annualised rates of return. All charts use a log scale.

series <- French("~/Downloads/French/", "F-F_Research_Data_Factors_daily_CSV.zip", frequency = "daily", price.series = TRUE) series <- zoo(series, as.Date(row.names(series))) plotseries(series, col = hcl.colors(n = 12, palette = "Dark 2"), log.scale = TRUE, labels = c("Market\n(excess return)", "SMB", "HML", "RF"))

The market (total return)

series <- French("~/Downloads/French/", "market", frequency = "daily", price.series = TRUE) series <- zoo(series, as.Date(row.names(series))) plotseries(series, col = hcl.colors(n = 12, palette = "Dark 2"), log.scale = TRUE, labels = c("Market"))

Momentum: portfolios weighted by market cap

series <- French("~/Downloads/French/", "10_Portfolios_Prior_12_2_CSV.zip", frequency = "monthly", weighting = "value", price.series = TRUE) series <- zoo(series, as.Date(row.names(series))) plotseries(series, col = hcl.colors(n = 30, palette = "Greens"), log.scale = TRUE, labels = colnames(series))

Momentum: portfolios equally weighted

series <- French("~/Downloads/French/", "10_Portfolios_Prior_12_2_CSV.zip", frequency = "monthly", weighting = "equal", price.series = TRUE) series <- zoo(series, as.Date(row.names(series))) plotseries(series, col = hcl.colors(n = 30, palette = "Greens"), log.scale = TRUE, labels = colnames(series))

Supported datasets

Invoking the function without any arguments results in a list of supported datasets.

French()

10_Portfolios_Prior_12_2_CSV.zip 10_Portfolios_Prior_12_2_Daily_CSV.zip 49_Industry_Portfolios_CSV.zip 49_Industry_Portfolios_daily_CSV.zip 6_portfolios_2x3_CSV.zip 6_portfolios_2x3_daily_CSV.zip F-F_Momentum_Factor_CSV.zip F-F_Momentum_Factor_daily_CSV.zip F-F_Research_Data_Factors_daily_CSV.zip ME_Breakpoints_CSV.zip Portfolios_Formed_on_BE-ME_CSV.zip Portfolios_Formed_on_NI_CSV.zip Portfolios_Formed_on_RESVAR_CSV.zip Portfolios_Formed_on_VAR_CSV.zip Siccodes10.zip Siccodes12.zip Siccodes17.zip Siccodes30.zip Siccodes38.zip Siccodes48.zip Siccodes49.zip Siccodes5.zip