Streaks in the US equity market

In this note we'll look into streaks – periods of uninterrupted price increases and decreases, a.k.a. bull and bear markets– in the US equity market.

We use data from Kenneth French's website at https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/ The dataset comprises daily data total-return data.

library("NMOF") library("zoo") P <- French(dest.dir = tempdir(), dataset = "market", frequency = "daily", price.series = TRUE, na.rm = TRUE) P <- zoo(P, as.Date(row.names(P))) str(P)

‘zoo’ series from 1926-06-30 to 2020-11-30 Data: num [1:24875, 1] 1 1 1.01 1.01 1.01 ... - attr(*, "dimnames")=List of 2 ..$ : chr [1:24875] "1926-06-30" "1926-07-01" "1926-07-02" ... ..$ : chr "Market" Index: Date[1:24875], format: "1926-06-30" "1926-07-01" ...

The data are complete: there are no missing values.

any(is.na(P))

[1] FALSE

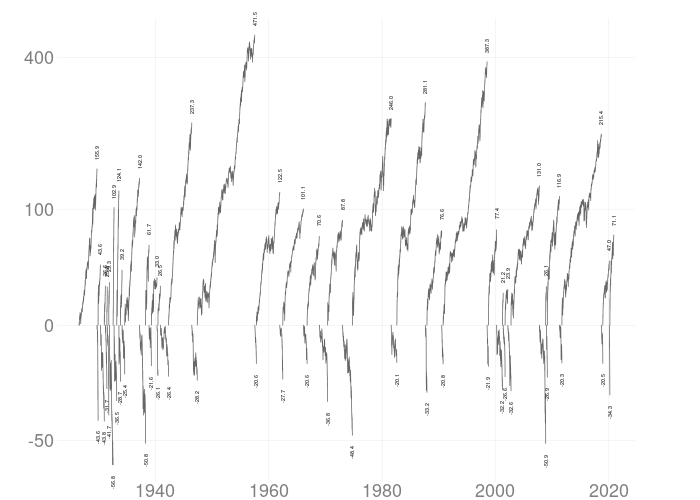

Function `streaks` in package PMwR computes series of uninterrupted up and down movements ('streaks') in a price series. Uninterrupted is meant in the sense that no countermovement of a certain percentage size or more occurs in up (down) movements. Th default is threshold is 20%.

library("PMwR") up.down <- streaks(P) str(up.down) head(up.down)

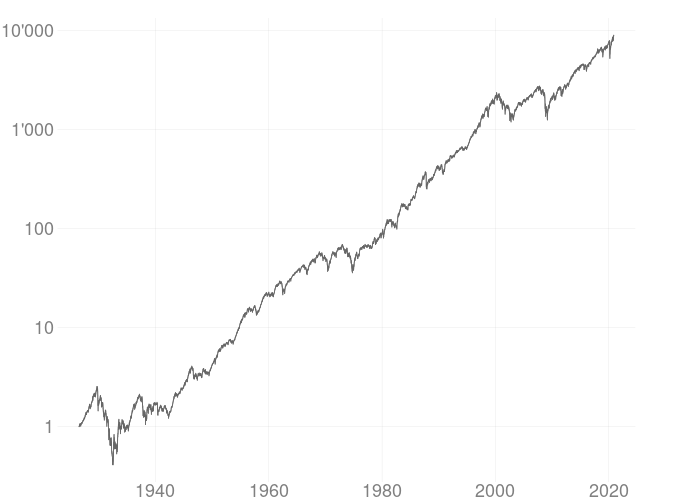

We can plot those streaks.

library("plotseries") par(cex.axis = 2) plotseries(P, log.scale = TRUE)

par(cex.axis = 2) plotseries(P, series.type = "streaks")