Path-dependent strategies

In this note I show how a simple path-dependent

strategy – a stop loss – can be implemented with

btest. To keep it simple, we look only at the

univariate case, i.e. a single time-series. For data,

we use the time-series of the DAX (a German

stock-market index), which is included in the PMwR

package.

library("PMwR") prices <- c(DAX[[1]]) timestamp <- as.Date(row.names(DAX))

The first strategy: buy once, on the first timestamp,

and then sell if the price moves more than stop.loss

percent below the entry price.

buy_once_SL <- function(stop.loss) { if (Time(0) == 1) { Globals$entry <- Close(0) 1 } else if (Portfolio() && Close() < Globals$entry * (1 - stop.loss)) 0 } bt.buy_once_SL <- btest(prices = prices, signal = buy_once_SL, timestamp = timestamp, stop.loss = 0.05, b = 0) journal(bt.buy_once_SL)

instrument timestamp amount price 1 asset 1 2014-01-02 1 9400.04 2 asset 1 2014-10-13 -1 8812.43 2 transactions

Remarks: Since we have a calendar schedule when to buy,

there is no need for a burnin, so b is set to zero.

Also, within the signal function, we test whether

Time(0) equals 1, i.e. we use no lag. The else

clause starts with the test Portfolio(): If we are

not invested (i.e. we have been stopped out), the

position will be zero, which evaluates to FALSE. For

this example, such a test would not have been

necessary, since the second condition is very fast to

compute. But in general, for a path-dependent

strategy, btest needs to loop through every single

data point, and then not doing unnecessary work helps

to speed up things.

Suppose we had wanted a trailing stop, i.e. sell when

stop.loss percent below the highest price observed

after the position was opened. In that case, we simply

would have to update the entry price (which should

then better be named high or reference or something

similar). This update would have to happen whenever we

have an open position. In any case, the entry is stored

in Globals, which is an environment provided by

btest. For our purposes, we can treat it just like a

list, only that it is never copied. Thus, the objects

we put into it are not local, but are persistent

between invocations of the signal function.

In the example above, once we have closed the position,

we will never again invest. Suppose that instead, we

would want to reinstate a new position at the first day

of every quarter. We would need only few changes to

buy_once_SL.

library("datetimeutils") trade.dates <- nth_day(timestamp, period = "quarter", n = "first") buy_quarterly_SL <- function(stop.loss, trade.dates) { if (Timestamp(0) %in% trade.dates) { Globals$entry <- Close(0) 1 } else if (Portfolio() && Close() < Globals$entry * (1 - stop.loss)) 0 } bt.buy_quarterly_SL <- btest(prices = prices, signal = buy_quarterly_SL, timestamp = timestamp, stop.loss = 0.05, trade.dates = trade.dates, b = 0) journal(bt.buy_quarterly_SL)

instrument timestamp amount price 1 asset 1 2014-01-02 1 9400.04 2 asset 1 2014-08-04 -1 9154.14 3 asset 1 2014-10-01 1 9382.03 4 asset 1 2014-10-13 -1 8812.43 5 asset 1 2015-01-02 1 9764.73 6 asset 1 2015-05-06 -1 11350.15 7 asset 1 2015-07-01 1 11180.50 8 asset 1 2015-08-21 -1 10124.52 9 asset 1 2015-10-01 1 9509.25 9 transactions

Note that with this specification, the entry price is

updated every quarter, even when we have not been

stopped out.

Finally, we may want to compare the results with a buy-and-hold strategy. The signal function is so simple that we can inline it.

bt.buy_hold <- btest(prices = prices, signal = function() 1, timestamp = timestamp, b = 0) journal(bt.buy_hold)

instrument timestamp amount price 1 asset 1 2014-01-02 1 9400.04 1 transaction

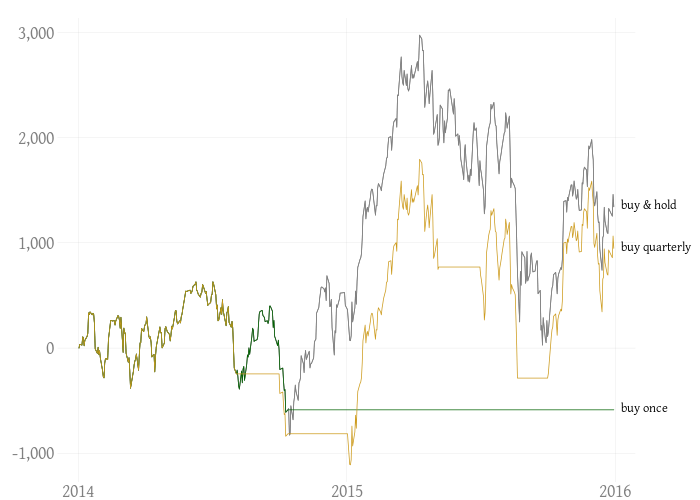

We plot the resulting equity curves.

library("plotseries") ## https://github.com/enricoschumann/plotseries library("zoo") plotseries(merge(as.zoo(NAVseries(bt.buy_hold)), as.zoo(NAVseries(bt.buy_once_SL)), as.zoo(NAVseries(bt.buy_quarterly_SL))), add0 = TRUE, add1 = FALSE, col = c(grey(0.5), "darkgreen", "goldenrod3"), labels = c("buy & hold", "buy once", "buy quarterly"), add.returns = FALSE, add.dollars = FALSE, big.mark = ",")